- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

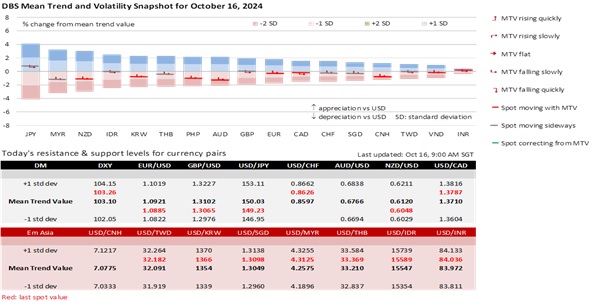

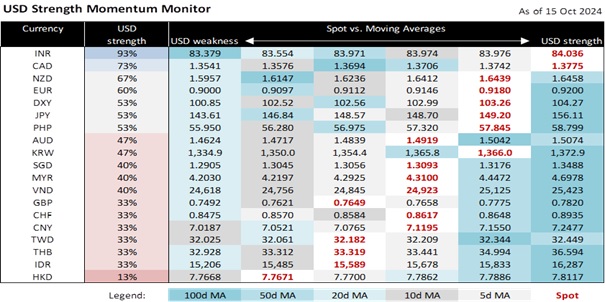

EUR/USD depreciated 0.2% to 1.0893 overnight before tomorrow’s European Central Bank meeting. Following the drop in the Eurozone’s CPI inflation to 1.8% YoY in September, the ECB will likely lower the deposit facility rate by 25 bps to 3.25%. However, this month’s short EUR/USD strategy risks running into a classic “buy the rumour, sell the fact” scenario. This month’s 2.2% depreciation has exceeded all monthly losses this year. Since November 2023, the 100-week moving average (currently around 1.0825) has significantly supported the EUR. Assuming this back-to-back cut materialises, the ECB may not pivot for another cut in December amid expectations for two Fed cuts in November and December. Eurozone’s core inflation, at 2.7% YoY in September, remained above the ECB’s 2% target. Economic pessimism also eased after the ZEW survey expectations improved to a six-month high of 20.1 in October, following three months of declines.

The DXY Index failed thrice over the past two days to trade above the significant resistance of around 103.30. The greenback was caught between two forces. On the one hand, the greenback reprised its haven role from a sell-off in semiconductor counters that pummelled the major US stock indices from record highs. On the other hand, the dollar’s haven appeal was offset by US bond yields accompanying the decline in equities. The US Treasury 10Y yield tumbled to 4.03% after it held a 4.06-4.12% range in the previous two sessions. San Francisco Fed President Mary Daly played down the recent better-than-expected US nonfarm payrolls and CPI inflation data. As the Fed’s renowned labour economist, Daly believed the US job market was no longer a major source of inflation pressures, adding that firms found it difficult to pass on price increases. Despite last month’s 50 bps cut, interest rates were still restrictive and a long way from neutral, working to lower inflation to its 2% target.

Meanwhile, Brent crude oil prices fell a third day by 3.8% to USD74.52 per barrel, its lowest level since October 2. OPEC and the International Energy Agency lowered their forecasts for global oil demand in 2024, citing oversupply amid weak demand from China. Fears of a broader conflict in the Middle East eased after Israeli Prime Minister Benjamin Netanyahu assured US President Joe Biden that it would strike military and not target oil or nuclear sites in Iran. On October 13, US Secretary of State Antony Blinken and Defense Secretary Lloyd Austin sent a signed warning letter to Israel to address, over the next 30 days, the significant drop in humanitarian aid into Gaza or risk a cut in arms sales. Although the deadline comes after the US Presidential Elections on November 5, the new President will only take over the White House in January 2025.

Against this background, the commodity-led currencies – AUD, NZD, and CAD – appear vulnerable, with the JPY viewed as a possible alternative haven to the greenback. Markets are hesitant to take USD/JPY above 150 for the rest of the month. The Bank of Japan is expected to affirm its rate hiking framework at its meeting on October 31, after Japan’s snap election on October 27. Polls indicate a victory for the ruling Liberal Democrat Party with a reduced majority.

Quote of the Day

“I only hope that we don’t lose sight of one thing – that it was all started by a mouse.”

Walt Disney

October 16 in history

The Walt Disney Company was founded in 1923.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.