- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

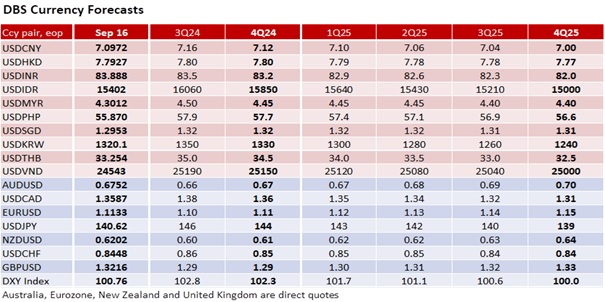

The DXY Index depreciated a third session by 0.4% to 100.76, approaching 100.55, the year’s weakest close on August 27. The futures market has increased the probability of a 50 bps rate cut at the September 18 FOMC meeting to 170% from 118% last Wednesday. Over the same period, the US Treasury 2Y yield eased by 9.1 bps to 3.551%, while the 10Y yield fell 3.6 bps to 3.618%. Conversely, economists polled by Bloomberg expect the Fed to mirror its peers and commence with a 25 bps reduction.

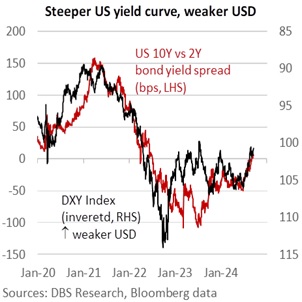

US National Economic Council Director Lael Brainard backed the latter in her remarks to the Council on Foreign Relations on Monday. Brainard, a former Fed Vice Chair, reinforced the Fed’s assessment that the inflation was coming back down to normal levels without considerable dislocation in the labour market amid a sustained economic expansion. She attributed the inflation surge to supply chain shocks and disruption of commodities instead of overall excess demand. Expect Fed Chair Jerome Powell to emphasize tomorrow that the Fed was reducing top-level restriction in monetary policy to safeguard the labour market progress, downplaying the market’s recession fear linked to rising unemployment. Hence, the DXY could eventually move into a lower 90-100 trading range now that the UST yield curve (10Y vs. 2Y differential) was no longer inverted with scope to become more positively sloped.

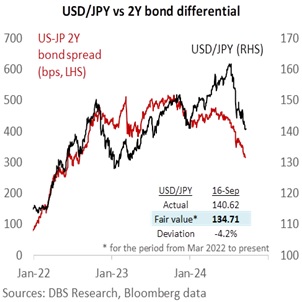

USD/JPY traded briefly below 140, hitting 139.58 during the Asian session, before ending 0.2% lower at 140.62 overnight. Japan’s government bond yield differentials vs. the US continued to narrow, implying scope for USD/JPY to eventually trade in a lower 135-140 range. The Bank of Japan is set to reaffirm its commitment to keep raising interest rates through 2025 at its September 20 meeting, two days after the Fed delivers its first rate cut. Having attributed last month’s market volatility to US recession fears on a rising unemployment rate, BOJ Governor Kazuo Ueda will unlikely heed the call for restraint in raising rates by a leading candidate in the Liberal Democratic Party (LDP) party leadership race. Markets will scrutinize the Fed’s Summary of Economic Projections for upward revisions in the US unemployment rate forecasts north of 4.1% to lower the projected appropriate policy path for the Fed Funds Rate to the 3.6% projected last December vs. the 3.9% forecast in June.

Quote of the day

“The President made a clear commitment to respect the independence of the Federal Reserve in fighting inflation. This was an important contrast to his predecessor, who repeatedly criticized Federal Reserve monetary policy during the previous administration.”

Lael Brainard

September 17 in history

In 1683, Dutch scientist Antonie van Leeuwenhoek was first to report the existence of bacteria.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.