- Banking

- Wealth

- NRI Banking

- Customer Services

Related Insights

The DXY’s outlook has become less predictable after its aggressive sell-off in the first half of July. Despite its intention to lower interest rates this year, the Fed lacks the confidence to provide time-based guidance. With the Fed in a blackout period this week, pay attention to Thursday’s US advance GDP and Friday’s PCE deflators to affirm the futures market’s bet for a Fed cut in September.

Given the relatively weaker high-frequency US data in April-June vs. the previous three months, we cannot rule out GDP missing the consensus for growth to improve to an annualized 1.9% QoQ saar in 2Q24 from 1.4% in 1Q24. The Fed will likely consider the PCE headline and core inflation as very good if June repeats the 0% MoM and 0.1% readings in May. However, the Fed appeared more ready to cut rates if the labour market weakened unexpectedly, i.e., the unemployment rate rises to 4.1% in June. Unfortunately, the US monthly jobs report will only be out on August 2, after the FOMC meeting on July 30-31.

The market is also grappling with how a Trump victory in the US Presidential election in November will influence the USD. Those who favour a stronger USD argue that Trump’s trade tariffs on China and tax cut plans will fuel inflation and higher interest rates in America. However, the UK mini-budget crisis in September-October 2022 demonstrated how an unsustainable fiscal situation could hurt a currency. Although Trump’s running mate, JD Vance, called China the biggest threat to the US, Trump would welcome China to build cars in the US and did not like the USD’s strength, especially against the JPY and CNY.

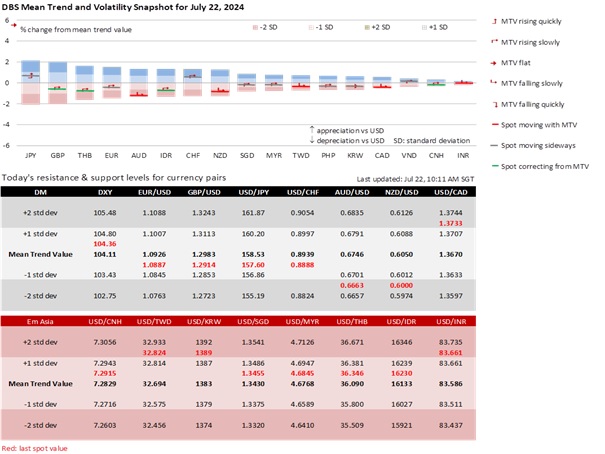

On Friday, we do not rule out the Monetary Authority of Singapore slightly easing the slope of its SGD NEER policy band. We see tomorrow’s MAS Core inflation slowing to 3% YoY in June after holding at 3.1% for three months. If so, core inflation would fall to 3.1% in 2Q24 from 3.3% in 1Q24. CPI and core inflation have been within this year’s official forecast range of 2.5-3.5% since March. According to our model, the SGD NEER has eased from the upper quartile towards the mid-point of its policy band, consistent with the MAS’s comment about core inflation staying on its disinflation path and easing more significantly in 4Q24 before reaching 2% in 2025.

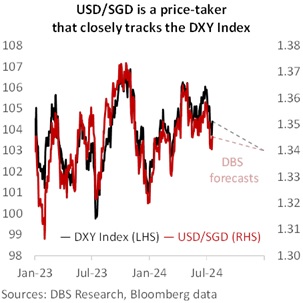

Despite this, USD/SGD is significantly correlated with the DXY Index. In the first half of July, USD/SGD’s fall from 1.36 to 1.34 mirrored the DXY’s drop from 106 to 103.5. To push lower, USD/SGD and the DXY will need the Fed to become more confident about rate cuts.

Quote of the day

”The essence of investment management is the management of risks, not the management of returns.”

Benjamin Graham

22 July in history

In 2019, India's lunar mission, Chandrayaan-2 successfully took off from Satish Dhawan Space Center, Sriharikota aiming to be fourth nation to soft-land on the moon.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.