- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

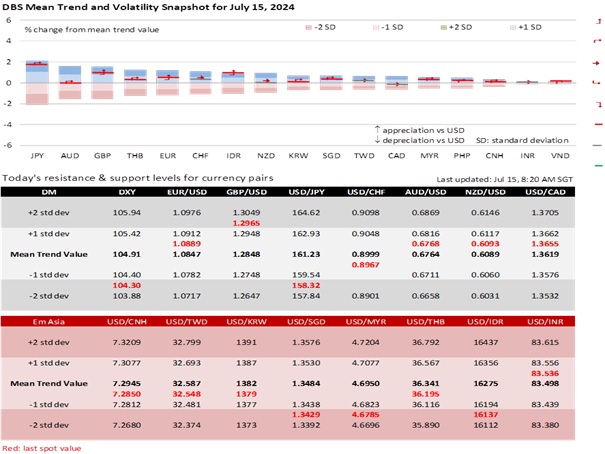

The DXY Index depreciated 1.7% in the first fortnight of July to 104.09, back to early June lows. The greenback is under pressure from the futures market, increasing the probability that the Fed will start lowering rates in September to 94.5% vs. 56.5% at the last FOMC meeting on June 12. Fed officials have become more confident about US inflation resuming its decline after a sticky first quarter. CPI inflation fell a third month and posted its first negative month-on-month reading since May 2020. The Fed’s favourite inflation gauges, the PCE deflators, should mirror the softer CPI readings. PCE inflation fell to 2.6% YoY in May, hitting the Fed’s forecast for 4Q24. Core inflation was more impressive by declining to 2.6%, below the Fed’s 2.8% forecast.

Today, Fed Chair Jerome Powell will focus on “balanced risks” during his interview at the Economic Club of Washington DC. Powell will likely be less concerned about reducing rates too soon without reigniting inflation while acknowledging that lowering them too late could lose the economic expansion. The US unemployment rate extended its rise to 4.1% in June after hitting 4% in May, the Fed’s forecast for 4Q24. During his semi-annual testimonies last week, Powell told US lawmakers that the Fed could respond if the US labour market weakened unexpectedly in a material way.

Assuming the US inflation and jobs data keep moving as they have, the Fed could become to be less neutral at the FOMC meeting on July 30-31 and affirm a bias to lower rates in September at the Kansas City Fed’s Jackson Hole Symposium on August 22-24. We maintain our view that the Fed should start lowering rates every quarter from 3Q24 through 4Q25.

Meanwhile, the USD is clawing back some of its losses on the “Trump Trade” after the failed assassination attempt on the Republican presidential candidate, Donald Trump. With President Joe Biden losing support from Democrats for his re-election bid, polls are skewed towards Trump at the US Presidential elections on November 5. However, we are sceptical about a replay of the USD’s rally into Trump’s victory in the 2016 elections. Today, the Fed is looking to lower rates after a hiking cycle and not at starting a two-year hiking cycle in December 2016. The fiscal situation has become unsustainable after persistent budget deficits during the Trump and Biden terms. The Congressional Budget Office projected the federal debt held by the public exceeding 100% of GDP in 2025 from 75% in 2015. DXY plunged almost 10% in 2017 during the first year of Trump’s presidency from political uncertainties in the US amid more economic optimism in Europe and emerging markets.

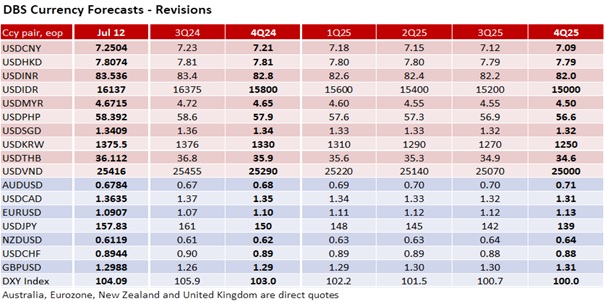

We have lifted our end-2024 target for USD/CNY to 7.21 from 7.12. The People’s Bank of China (PBoC) raised the daily fixing from 7.0950 at the end of 1Q24 to 7.1315 last Friday. The central bank is gradually shifting monetary policy from quantitative targets towards interest rates. The PBOC is studying how to carry out government bond trading in the secondary market with the finance ministry without being seen as adopting quantitative easing. Year-to-date, the 10Y bond yield declined by 30 bps in China vs. a 30 bps increase in the US, while the SPX 500 rallied 17.7% vs. a slight 1.2% gain in the CSI 300 Index. However, we expect the USD to decline against the CNY when the Fed cut cycle begins.

Quote of the day

“Assassination is the extreme form of censorship.”

George Bernard Shaw

15 July in history

Boeing Company (Pacific Aero) was formed by William Boeing in Seattle, Washington USA, in 1916.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.