- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

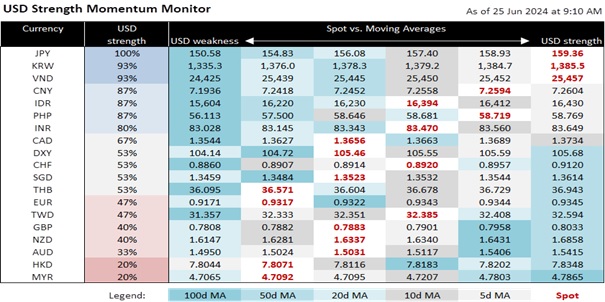

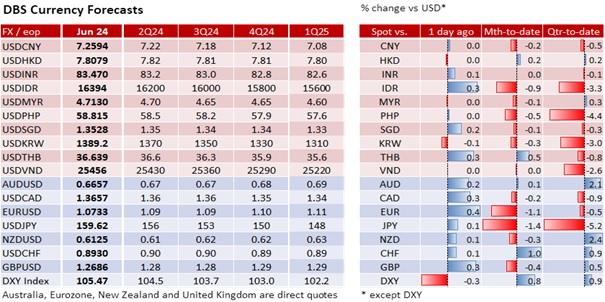

USD/JPY started Monday higher, near 160, but ended the session lower at 159.62. Japan’s Vice Minister of Finance for International Affairs Masato Kanda said the US Treasury Department’s decision to add Japan to the monitoring list had “absolutely no impact” on its resolve to address the excessive currency speculation. Kanda clarified that Japan’s interventions did not seek to gain an unfair competitive advantage in international trade via a weaker exchange rate but to prevent excessive JPY depreciation that hurts Japan’s companies and households. Moving against falling US bond yields, the 10Y JGB yield firmed a third session by 2.1 bps to 0.996% in anticipation of more details regarding the Bank of Japan’s plan to trim bond purchases at July’s meeting. Hence, we cannot dismiss the downside risks in USD/JPY.

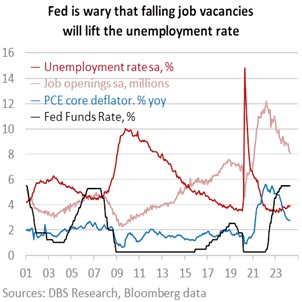

The DXY Index shed 0.3% to 105.47 on a 2.3 bps drop in the US 10Y bond yield to 4.23% ahead of the slower US PCE inflation data expected this Friday. The Fed is reminding markets of its dual mandate. San Francisco Fed President Mary Daly said the Fed is open to holding interest rates high for longer on sticky inflation or lowering them on rising unemployment rates. During the FOMC meeting on June 12, Fed Chair Jerome Powell said the Fed was ready to respond if jobs weakened unexpectedly and considered the recent higher unemployment rate as an important statistic. He will likely relay the same message during his semi-annual testimony on monetary policy to the US Senate Banking Committee on July 9.

Today, US Conference Board is expected to report a lower Consumer Confidence Index of 100 in June vs. 102 in May. It is crucial to pay attention to how consumers perceive employment prospects in the next six months. When the Fed announced its final hike in July 2023, the percentage of respondents who believed jobs were plentiful fell below those who thought jobs were scarce. This shift in perception is significant because Daly noted that falling job vacancies have started to lift the unemployment rate. Chicago Fed President Austan Goolsbee is also monitoring the rise in jobless claims and unemployment rate as signs that the US economy is no longer overheating, which could lead to a less restrictive policy if inflation slows and stays on track to return to its 2% target.

Quote of the day

“An owl is traditionally a symbol of wisdom, so we are neither doves nor hawks, but owls, and we are vigilant when others are resting.”

Urjit Patel

25 June in history

In 1950, North Korea invaded South Korea, starting the Korean War.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.