- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

- Relief rally continues amid lingering uncertainty 25 Apr 2025

- The USD’s relief rally masks a tug-of-war ahead 23 Apr 2025

- The USD is hurting on the inside 22 Apr 2025

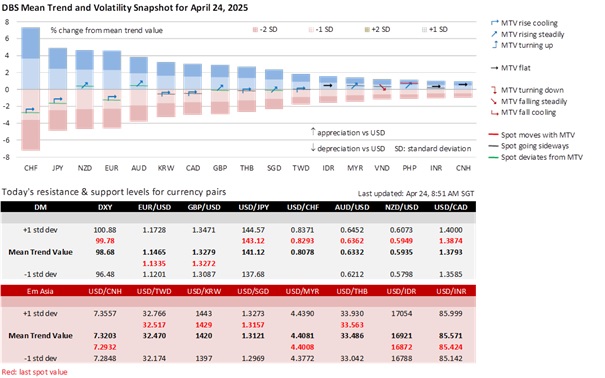

USD/CHF broke below its two-year range between 0.84 and 0.92 this month. USD/CHF hit a decade-low of 0.8040 on April 21 before recovering to 0.83 in the past two sessions. Before attempting to predict if USD/CHF has bottomed, it will be useful to revisit the previous episodes when USD/CHF hit even lower levels in 2011 and 2015 to provide a better understanding of the CHF’s strength and how the Swiss National Bank responded in each case.

In the first episode, USD/CHF bottomed at 0.7071 in August 2011. SNB targeted EUR/CHF, which was falling towards 1.00 in August 2011, from investors seeking safety during the Eurozone sovereign debt crisis. In August 2011, markets heeded the SNB’s warning that the CHF was “massively overvalued” after it lowered interest rates to near 0% and expanded liquidity operations. In September 2011, the SNB declared it would “no longer tolerate” a EUR/CHF rate below 1.210 and was prepared to buy unlimited foreign currency to enforce this minimum rate. USD/CHF rose over the next year to a high of 0.9970 in July 2012.

In the second episode, USD/CHF bottomed at 0.7406 in January 2015. On January 15, 2015, the SNB made a shock announcement to abandon the EUR/CHF peg at 1.20. EUR/CHF crashed to 0.85, pummelling USD/CHF to 0.74 that day. The SNB was pre-empting the European Central Bank, which unveiled an expanded asset purchase programme a week later, which heralded the formal start of QE operations in March 2015. However, the SNB’s shock announcement damaged its credibility, forcing an immediate response to cut interest rates further into negative territory, from -0.25% to -0.75%, to counter the CHF’s excessive appreciation. USD/CHF recovered to 1.00 in mid-March 2015 before holding a 0.94-1.03 range from 2016 to 2017.

What were the insights from these two episodes? The CHF’s strength stemmed from its haven status to Eurozone risks. The prevailing USD strength in past episodes became part of the solution when the SNB cut interest rates and intervened in the forex market to counter the CHF’s appreciation.

Similar factors were also in place when the SNB countered the CHF’s haven status during the Trump Trade in late 2024. Shortly after assuming office in October 2024, SNB Chairman Martin Schlegel warned in November 2024 that the central bank could counter the CHF’s haven status through negative interest rates if needed and FX interventions. EUR/CHF had depreciated to 0.93 on a stronger USD on Trump’s victory in the November 2024 US elections. In December 2024, SNB slashed interest rates by 50 bps to 0.50% amid USD strength, which lifted USD/CHF to near 0.92 in January 2024 from its 0.84 low in September 2024.

Unfortunately, the landscape has become less conducive to countering the CHF’s strength in 2025. The USD’s “Trump Trade” rally faltered after Trump’s inauguration on January 20. The SNB’s 25 bps rate cut to 0.25% on March 20 briefly supported USD/CHF around 0.88 but was overshadowed by Trump’s erratic and unpredictable tariff policy. However, Trump’s challenge to the Fed’s independence undermined one of the sacred institutional pillars supporting the USD’s hegemony and its haven role. The subsequent elevation in the CHF’s haven status drove USD/CHF to a decade-low of 0.8040 on April 21.

Given Trump’s history of policy reversals, it is premature to conclude that USD/CHF’s rebound to 0.83 over the past two sessions is sustainable. There is no assurance that Trump will refrain from threatening Powell again as he seeks lower borrowing costs to support his administration’s push for extending his 2017 tax cuts by Independence Day. With the IMF’s latest 2025 growth forecast for the US economy aligning closely with the Fed’s projection, Powell will likely maintain the Fed’s extended rate pause stance on inflation risks driven by Trump’s tariffs. However, if advance GDP growth for 1Q25 turns negative – as projected by the Atlanta Fed GDPNow model – Trump will likely attack Powell again. Caution is also warranted regarding the Trump administration’s offer to reduce tariffs on Chinese imports. Any meaningful de-escalation would require Trump and China President Xi Jinping to resume direct engagement to lay the groundwork for trade negotiations first.

Without EUR/USD falling below 1.11 or the DXY Index rising above 1.01 again, USD/CHF will struggle to re-enter its previous two-year range of 0.84-0.92.

Quote of the Day

“There are three kinds of brains: One understands of itself, another can be taught to understand, and the third can neither understand to itself or be taught to understand.”

Niccolo Machiavelli

April 24 in history

The Hubble Space Telescope was launched in 1990.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- Relief rally continues amid lingering uncertainty 25 Apr 2025

- The USD’s relief rally masks a tug-of-war ahead 23 Apr 2025

- The USD is hurting on the inside 22 Apr 2025

Related Insights

- Relief rally continues amid lingering uncertainty 25 Apr 2025

- The USD’s relief rally masks a tug-of-war ahead 23 Apr 2025

- The USD is hurting on the inside 22 Apr 2025