- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

- FX Tactical Ideas: USD in a Corrective Rebound 28 Mar 2025

- USD eases on hopes of “lenient” reciprocal tariffs 28 Mar 2025

- Less sanguine as Trump’s tariff impact weighs 27 Mar 2025

US-led recession fears should see investors seeking safety in the greenback and US bonds. US President Donald Trump warned that reciprocal tariffs would hit all countries on April 2, or “Liberation Day.” Trump added that he “couldn’t care less” if his 25% tariff on autos leads US automakers to raise prices. Many Developed Market countries have threatened retaliation, increasing the odds of a global trade war that would hurt world economic growth.

The Atlanta Fed GDPNow model predicted that US GDP growth would contract by 2.8% QoQ saar in 1Q25, driven primarily by a surge in US imports to beat Trump’s tariffs. While the model saw US consumer and government spending weakening, it expected domestic demand growth to remain positive. Unless this Friday’s US monthly jobs disappoint significantly, Fed officials see Trump’s tariffs posing a greater risk to inflation than growth, advocating holding rates steady for an extended period. Instead, the Fed will, starting in April, reduce the monthly redemption cap on US Treasuries to USD5 bn from USD 25bn to provide additional liquidity and support to the financial system during this period of heightened uncertainty.

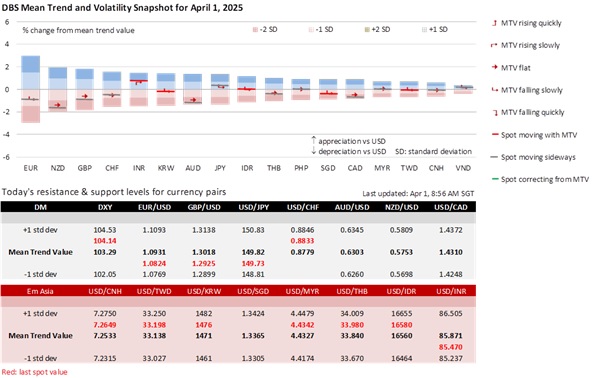

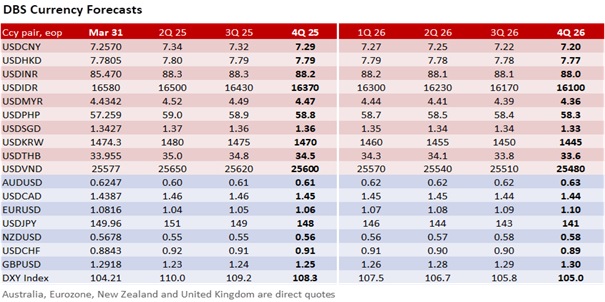

Against this background, the risk has increased for USD/JPY to stay above instead of below 150. The JPY’s strength this quarter from the Bank of Japan rate hike expectations has given way to Prime Minister Shigeru Ishiba’s worries about Trump’s auto tariff having a “very big” impact on Japan’s economy. The US is Japan’s largest export market, and its autos and auto parts account for a third of its exports to the US.

The commodity-led currencies – AUD, NZD, and CAD – should keep underperforming as they did over the past week ahead of Trump’s reciprocal tariffs. Canada has taken a notable assertive stance in responding to US tariffs under the leadership of new Prime Minister Mark Carney. The Reserve Bank of Australia is expected to pause today after February’s rate cut. However, it may pave the way for a cut at the May 20 meeting after Australia’s national elections on May 3. The Reserve Bank of New Zealand is anticipated to lower rates at its April 9 meeting; the next 25 bps cut to 3.50% will bring the cumulative easing since August 2024 to 200 bps. Despite the surprise rebound in GDP growth to 0.7% QoQ sa in 4Q24, the RBNZ has emphasized continued monetary support to ensure sustained economic recovery.

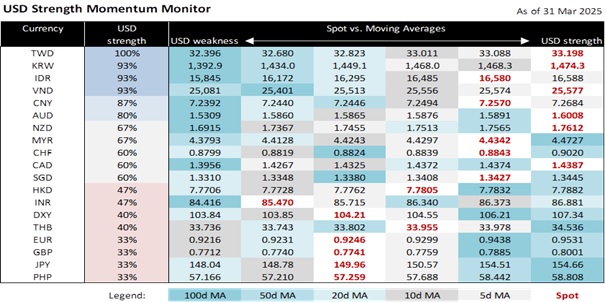

Currencies such as the KRW, TWD, and SGD have underperformed their Asian peers in the past week because of their heavy reliance on international trade. After failing to break below the support around 1430, USD/KRW returned near its 16-year high of 1478.60 at the end of 2024. South Korea is exposed to Trump’s tariffs on autos and steel. USD/TWD hit a 9-year high of 33.198 at the end of 1Q25. Taiwan has been identified among the “Dirty 15” countries with significant trade surpluses with the US; its significant semiconductor industry will unlikely be spared from US tariffs despite investments in US facilities. USD/SGD has risen towards 1.3450 in the past fortnight. It failed to break below the 1.33 support level this month after CPI and core inflation fell below their official forecast ranges for this year.

Quote of the Day

“There is no such uncertainty as a sure thing.”

Robert Burns

April 1 in history

The Malayan Union officially came into existence in 1946, was dissolved two years later, and replaced by the Federation of Malaya in 1948.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- FX Tactical Ideas: USD in a Corrective Rebound 28 Mar 2025

- USD eases on hopes of “lenient” reciprocal tariffs 28 Mar 2025

- Less sanguine as Trump’s tariff impact weighs 27 Mar 2025

Related Insights

- FX Tactical Ideas: USD in a Corrective Rebound 28 Mar 2025

- USD eases on hopes of “lenient” reciprocal tariffs 28 Mar 2025

- Less sanguine as Trump’s tariff impact weighs 27 Mar 2025