- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

- US exceptionalism challenged with rising trade tensions 13 Mar 2025

- Recalibrating our FX forecasts 12 Mar 2025

- US recession fears and “ReArm EU” hurdles 11 Mar 2025

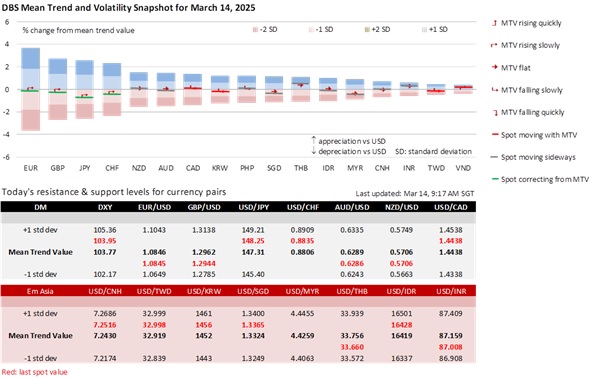

EUR/USD depreciated for a second day by 0.3% to 1.0857, driven by Germany’s political challenges to pass a substantial spending plan amid escalating EU-US trade tensions. The European Commission’s “ReArm Europe” Plan, which bolstered the EUR by 4.4% in the first week of March, faces several challenges. Germany’s CDU/CSU and the Social Democrats are engaged in intensive negotiations with the Greens to reach a compromise on reforming the debt brake to enable increased spending on defence and infrastructure. They aim to expedite a Bundestag vote on March 18th and Bundesrat approval on March 21st. The CDU/CSU, Social Democrats, and the Greens lack the two-thirds majority in the new Bundestag, which starts on March 25th, due to strong gains by the far-right and left parties.

The AfD has filed a motion with the Constitutional Court to challenge the legality of the plan to convene the outgoing Bundestag to push the spending package. Meanwhile, Fitch warned that the “ReArm Europe” Plan would lower the EU’s triple-A debt rating headroom because of the additional debt at the EU level.

More importantly, an EU-US tariff spat has emerged. The European Union retaliated against Trump’s 25% tariffs on steel and aluminium imports that took effect on March 13th. The European Commission announced tariffs on USD19.6bn of US goods, set to take effect between April 1st and 13th. Responding to the EU’s 50% tariff on American whiskey, Trump threatened a 200% tariff on all EU alcoholic products.

USD/CHF languished in a 0.88-0.8850 range for a second day after rising from a three-month low of 0.8758 on March 10th. We expect the Swiss National Bank to lower rates for the fifth time by 25 bps to 0.25% at the March 20th meeting. Due to a strong CHF and a sluggish economy, February CPI and core inflation were subdued at 0.3% YoY and 0.9%, respectively. On March 1st, the SNB expressed openness to forex interventions to counter the CHF’s haven status and indicated readiness to reintroduce negative interest rates if necessary to keep inflation within the official 0-2% target. The SNB forecasted the Swiss economy to expand by 1-1.5% in 2025. However, a lot has changed since March 1st. The EU economy is pulled in both directions from the US-EU tariff spat against heightening global trade tensions and the European Commission’s proposal for a “ReArm Europe” Plan. The OIS market suggests that this could be the final cut for the year, reflecting an expectation that the SNB will await greater clarity amid heightened uncertainties.

GBP/USD appreciated by 0.2% to 1.2950 in the first four days of this week, showing weaker momentum compared to the 2.7% rise in the first week of March. We expect the Bank of England to keep the bank rate unchanged at 4.50% at its March 20th meeting. Following a 25 bps cut on February 6th, CPI inflation rebounded to 3% YoY in January from 2.5% in December. Inflation should rise again in April due to higher National Insurance contributions by employers. Per the BOE’s guidance, inflation may reach 3.7% by 3Q 2025 before gradually returning to the 2% target by 4Q 2027. Services inflation, which the BOE uses to gauge underlying inflationary pressures, increased to 5% from 4.4%. However, the BOE has also adopted a cautious stance regarding the substantial risks posed by global trade tensions to the UK and global economies.

GBP bulls will be wary of the Spring Budget scheduled for March 26th, as the GBP10 billion headroom in Chancellor of the Exchequer Rachel Reeves’ Autumn Budget has been eroded by persistent inflation and sluggish growth. The Office for Budget Responsibility’s economic and fiscal forecasts will be crucial in determining the extent of necessary tax increases and spending cuts to adhere to the fiscal rules.

Quote of the Day

“I’m very proud of my gold pocket watch. My grandfather, on his deathbed, sold me this watch.”

Woody Allen

March 14 in history

The Gold Standard Act became effective in 1900, defining the USD by gold weight and requiring the US Treasury to redeem, on demand and in gold coin only.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- US exceptionalism challenged with rising trade tensions 13 Mar 2025

- Recalibrating our FX forecasts 12 Mar 2025

- US recession fears and “ReArm EU” hurdles 11 Mar 2025

Related Insights

- US exceptionalism challenged with rising trade tensions 13 Mar 2025

- Recalibrating our FX forecasts 12 Mar 2025

- US recession fears and “ReArm EU” hurdles 11 Mar 2025