- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

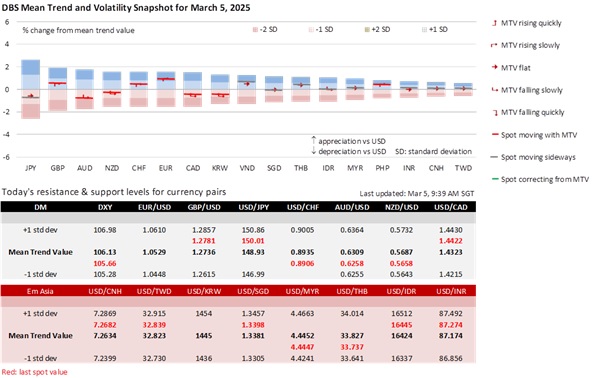

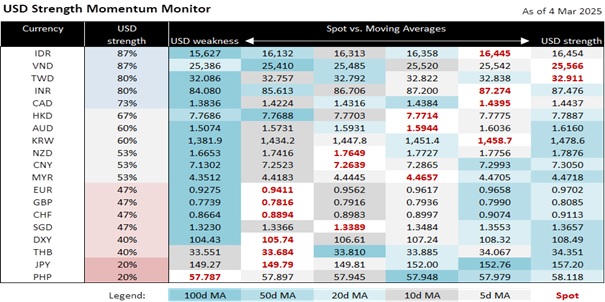

The greenback was not spared from tariffs unravelling the Trump Trades. Following US President Donald Trump’s decision to proceed with tariffs on Canada, Mexico, and China, US stagflation worries lowered the S&P 500 Index by 1.2% to 5778, its lowest level since the US elections on November 4. The DXY Index depreciated 1.1% to 105.56, its worst level since November 8, nearer the 103.89 level seen on November 4. Trump chided Japan and China for putting US goods at an unfair disadvantage through their weaker currencies. China has been keeping the USD/CNY fixing stable (averaging 7.18) since mid-November, while USD/JPY has been declining since the start of the year to below 150.

US Treasury Secretary Scott Bessent shrugged off Wall Street’s sell-off as temporary, adding that the focus was on Main Street and the rebalancing of the US economy. US Commerce Secretary Howard Lutnick hinted that Trump may offer some relief to companies that abided by the existing USMCA trade agreement. Even so, neither secretary played down the coming tariffs on steel and aluminium on March 12, the reciprocal tariffs from April 2, and other proposals on autos, semiconductors, pharmaceuticals, copper, lumber, and the EU. They also welcomed plans by a Taiwanese chipmaker and a Japanese automaker to build factories in the US to avoid tariffs.

Hence, it remains to be seen if any Trump compromise on tariffs on Mexico and Canada would be enough to fend off Mexico’s plan to retaliate with tariffs on Sunday. Canada struck back with an initial 25% tariff on CAD30bn of US imports, promising more levy on an additional CAD125bn three weeks later. China’s response has been measured and focused mainly on US agricultural and farm products. Today, China is expected to set this year’s growth target around 5% after vowing to fight to the “bitter end” a trade war with the US.

However, US inflation worries lifted the US Treasury 10Y yield by 8.9 bps to 4.24%. New York Fed President John Williams subscribed partially to half the market’s stagflation worries. Williams paid attention to the recent increase in inflation expectations driven by tariffs and signalled his intention to keep rates on hold at the upcoming FOMC meeting on March 18-19. Williams did not buy into US recession fears, merely acknowledging that GDP growth would slow from last year’s 2.8% level. Nonetheless, Williams’ faith in the resilience of the US economy would need to be substantiated by today’s ISM Services PMI, which consensus reckoned would slow to 52.5 in February from 52.8 in January. Prices paid is expected to remain unchanged at 60.4 while new orders increase to 51.5 from 51.3. Employment is expected to mirror the fall in manufacturing PMI to 51.6 from 52.3. While markets expect today’s ADP employment to slow to 140k in February from 183k in January, they see Friday’s nonfarm payrolls rising to 160k from 143k. Hence, it remains doubtful that the Fed will subscribe to the market’s three rate cut projection when it deliberates its Summary of Economic Projections.

The situation remains fluid, with global trade tensions continuing to shape market sentiment and economic expectations. While tariffs have triggered US stagflation worries and pressured the USD, markets will continue to watch US economic data and policy responses to gauge whether the US economy can absorb these shocks without derailing growth. If so, Trump’s protectionist-driven efforts to tilt supply chains back towards the US should lead to higher inflation that keeps US yield differentials wide in favour of the USD.

Quote of the Day

“True genius resides in the capacity for evaluation of uncertain, hazardous, and conflicting information.”

Winston Churchill

March 5 in history

Piano company Steinway & Sons was founded in 1853.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.