- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

Related Insights

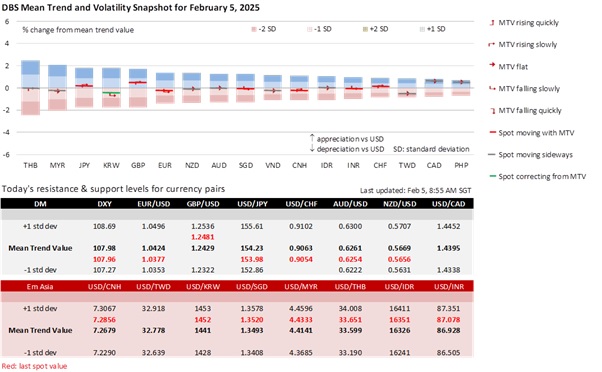

GBP/USD’s recovery will likely stall around 1.25, its significant resistance level this year. The GBP’s gain in the past two sessions was largely driven by the USD’s downward correction following the 30-day delay in Trump’s tariffs on Canadian and Mexican imports into the US. However, hopes for a similar de-escalation in US-China trade tensions faded after US President Donald Trump cancelled his phone call with China President Xi Jinping. This came in response to China’s retaliatory tariffs, which take effect on February 10, countering Trump’s 10% tariffs on Chinese imports on Tuesday.

We remain cautious about the optimism for the UK to avoid US tariffs. While the US does not have a goods trade deficit with the UK, it does have a significant services deficit. Trump’s recent comments – calling the UK “out of line” despite describing the UK’s trading relationship with the US as “fair and balanced” – suggested that negotiations may be needed to avoid tariffs. However, the UK’s stagnant economy remains vulnerable to Trump targeting tariffs on the fragile EU economy, which is the UK’s largest trading partner.

Against this background, the Bank of England will likely lower the bank rate by 25 bps to 4.50% at its February 6 meeting. This move would bring the UK’s policy in line with the upper bound of the Fed Funds Rate. We will look for signals on whether the UK aligns more closely with the dovish European Central rather than the cautious Fed in its policy outlook.

The markets have not lowered their guard about fiscal slippage risk from UK Chancellor Rachel Reeve’s October Budget. Although the 10Y Gilt yield eased to 4.52% from its 4.89% peak in mid-January, it remained above the 4.35% level seen before the budget announcement. The Office for Budget Responsibility (OBR) is expected to downgrade its 2% growth forecast for 2025 – which stands well above the 1.2% consensus – in the upcoming Spring Budget Statement next month. Markets will keep worrying about a weaker UK growth outlook amid higher borrowing costs shrinking the GBP9.9bn fiscal buffer, putting the government’s ability to meet its self-imposed fiscal rules at risk.

Quote of the Day

“Hope is a good breakfast, but it is a bad supper.”

Francis Bacon

February 5 in history

The United States and the United Kingdom signed treaty for Panama Canal in 1900.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.