- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- Notion of “US exceptionalism” thrown off-course as policy uncertainties introduce financial and stagflation risks

- Signs of macro weakness on the rise with Atlanta Fed GDPNow now pointing to a -2.4% decline in GDP; And yet, Fed’s hands are tied as inflation stays stubbornly high

- Equities: Stay Neutral while pivoting away from crowded trades in US; Seek opportunities in Europe and China

- Bonds: Capitalise on any spike in yields to switch from cash into bonds as we pivot towards a cutting cycle. Stay up in quality with A/BBB with a duration barbell overweighting 2-3Y and 7-10Y bonds

- Gold: Overweight safe haven gold as volatility and uncertainty are tailwinds for bullion due to its non-market correlating characteristics

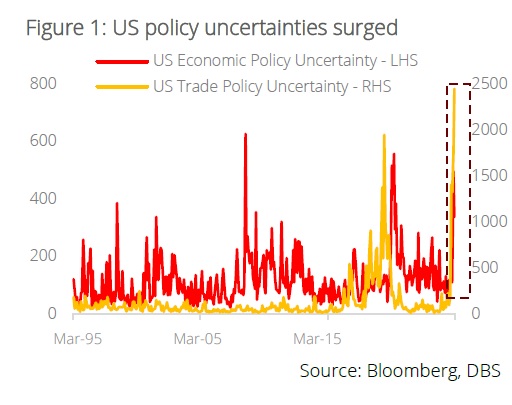

Policy chaos and growth fears triggered US selloff. Trump 2.0 has been a game-changer. All expectations of a continuation of “US exceptionalism” post-Trump’s election victory are now thrown off-course as the chaos of the new administration introduced acute financial and stagflation risks to the system. From the flip-flops on tariffs to the Transatlantic Alliance breakdown as the US dialed back on postwar American foreign policies and ceased being the “primary guarantor” for Europe’s security – these signal that the age of disruption has arrived, and market movements are clearly reflecting this paradigm shift.

Adding on to the proverbial wall of worries is the revival of growth fears as policy uncertainties hit an all-time high and weigh on both business and consumer confidence. ISM Manufacturing has fallen to 50.3 in February while the Atlanta Fed GDPNow is now pointing to a -2.4% decline in GDP. And yet despite the growth moderation, inflationary pressure remains stubbornly high, restricting the Fed’s ability to cut rates.

Make Europe Great Again; The pivot away from crowded trades. Trump’s “transactional” style of policy making and his undermining of the NATO alliance has clearly galvanised European leaders and created a European unity not seen in decades. Germany’s “Whatever It Takes” moment on the easing of fiscal conservatism is, perhaps, a telling moment that Europe-at-large is entering stimulus mode just when the US is engulfing itself with policy uncertainties. The implications for these shifts on portfolio construction are significant and our recommendations are:

Equities

- Stay Neutral on equities while pivoting away from crowded trades in the US. The very notion of “de-risking” from US equities is now a reality under the “America First” policy agenda. Funds are switching out of US given (i) the market’s valuation premium to rest of the world and (ii) expectations of a darkening economical and geopolitical mood.

- Seek opportunities in Europe (eg defence, financials). Germany’s "Whatever It Takes" moment in particular, translates to the end of fiscal conservatism and unleashes strong economic stimulus. According to Kiel Institute, GDP growth could increase by 0.9-1.5% per year if nations (i) increase defence spending to 3.5% of GDP (vs NATO's target of 2%) and (ii) purchase weapons manufactured domestically in Europe.

- Seek opportunities in China (eg technology). Investors are warming up to Chinese equities as DeepSeek’s technological breakthrough spurs a reconsideration of the market’s attractiveness (trading at steep valuation discount to the rest of the world).

- In the US, seek defensive exposure to healthcare while staying engaged on technology. Capitalise on volatility to add to core positions via structured products.

Bonds

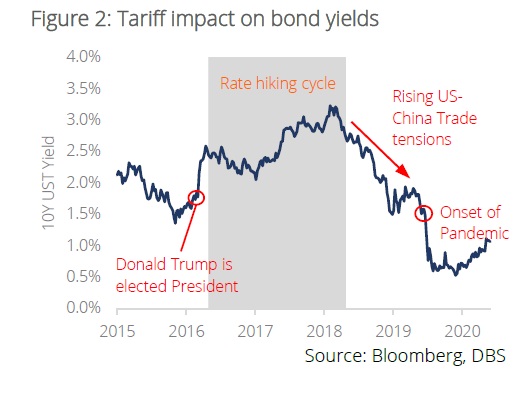

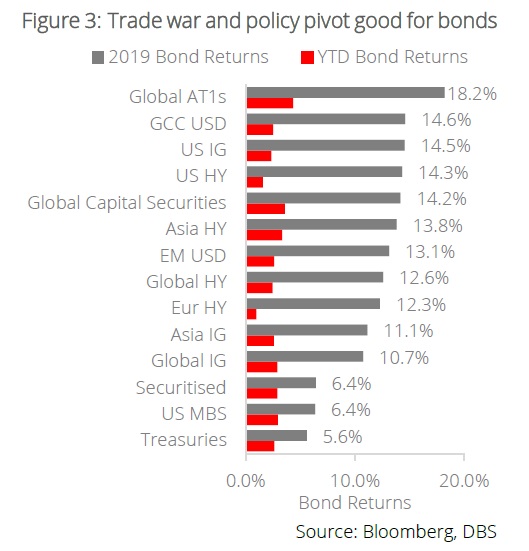

- We previously highlighted that a Trump presidency is not bond Kryptonite. Despite the market consensus that a Trump presidency may lead to a higher-and-higher yield environment due to tariff-driven inflation, our contrarian opinion was that it could also trigger a growth slowdown that conversely results in lower yields. We saw this play out in the previous round of tensions in 2019, and history appears to be repeating itself today.

- Investors should continue to capitalise on any spike in yields to switch from cash into bonds as we pivot towards a cutting cycle in global monetary policy. Stay up in quality with A/BBB and only make selective picks in BB that can weather a potential growth slowdown. Remain with a duration barbell – overweighting 2-3Y bonds to minimise cash reinvestment risk and 7-10Y bonds to capitalise on wider spread premiums.

Gold

- CIO has long touted gold as an important portfolio risk diversifier, and while 2024 played out extremely well for holders of bullion from a return perspective, 2025 has, thus far, been a better illustration of its role as an uncertainty and volatility hedge. Since the start of the year, markets have been roiled by tariffs, geopolitical conflicts, and the arrival of DeepSeek, but through it all, gold has remained resilient and even scaled new all-time highs.

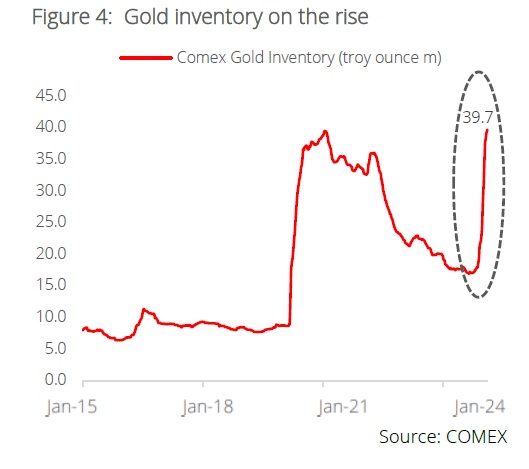

- Its role as an uncertainty hedge was put on display when gold staged a strong rally in January due to tariff fears. Worries that bullion, which has historically been exempt from import duties, might get tariffed in the future due to stockpiling on the New York commodities exchange. This led to a 127% increase in COMEX gold inventory levels since the US election in November last year.

- Amid the latest market sell-off on recession fears, gold has remained notably stoic, once again, reflecting its properties as a safe haven asset and store of value during times of market volatility. Should economic momentum wane, gold will also be well positioned for such a scenario as central banks will likely respond with rate cuts, which is typically a tailwind for gold.

Portfolio Approach: The best strategy in an era of volatility. The DBS CIO Barbell Strategy has outperformed S&P 500 and Nasdaq by 4.1 %pts and 9.1 %pts respectively this year, and this drives home the importance of embracing a portfolio approach in an era of heightened geopolitical and policy uncertainties. Our Overweight calls on gold and bonds are paying off handsomely this year as their resilience offset the volatility in equity markets.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.