- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

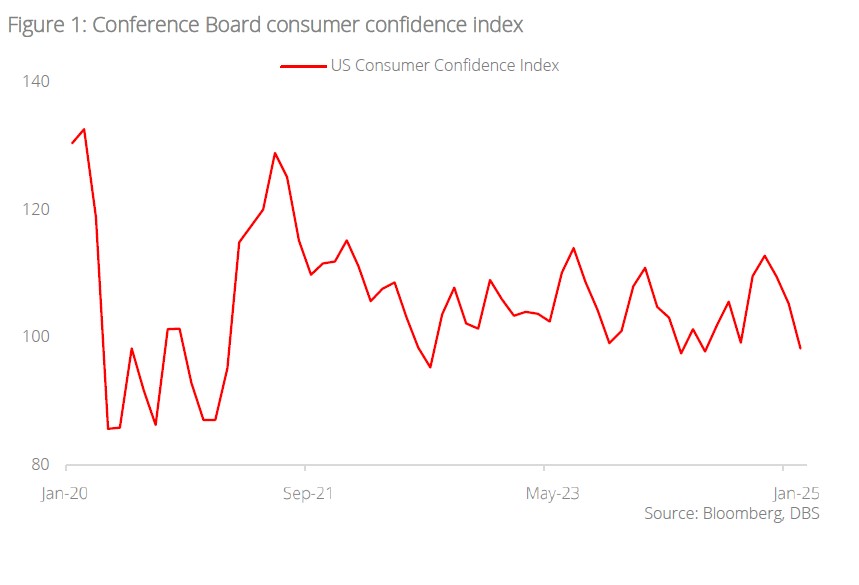

- US: Tariff tensions and declining consumer confidence are driving market uncertainty with expectations of Fed rate cuts and potential economic slowdown

- China: China’s economic resilience, driven by new bank loans and exports, is offsetting property market distress

- India: Economic growth is likely to rise, but tariff tensions with the US persist

- Thailand: Monetary easing by the BOT to boost economic growth

US: Consumer confidence took a hit. The Conference Board consumer confidence index fell to 98.3 from 105.3 previously. This 6.6% m/m decline was the worst since Aug 2021. Consumers became pessimistic about future business conditions and less optimistic about future income. Pessimism about future employment prospects worsened and reached a ten-month high amid a significant decline in bullishness over the stock market. The proportion of consumers anticipating a recession over the next 12 months increased to a nine-month high. Fed cut bets have also been added and the market now sees two full cuts being delivered.

Inflation expectations over the next 12 months surged to 6% from 5.2% in January on the Trump administration’s policies. Notably, the mentions of trade and tariffs increased to a level unseen since 2019.

Real gross domestic product (GDP) increased at an annual rate of 2.3% in the fourth quarter of 2024 (i.e. October, November, and December), according to the second estimate released by the US Bureau of Economic Analysis. In the third quarter, real GDP increased 3.1%. The increase in real GDP in the fourth quarter is mainly due to increases in consumer and government spending. These increases were partly offset by a decrease in investment and imports.

However, Fed officials have adopted a wait-and-see approach to monetary policy. The next Federal Open Market Committee meeting on 18-19 March will be held after Trump’s tariffs on Canada and Mexico next week, assuming no additional delay. While noting that monetary policy has been modestly restrictive—enough to return inflation to its 2% target—Richmond Fed President Thomas Barkin cautioned that the Fed may need to lean against the inflationary headwinds from the Trump administration’s policies.

Download the PDF to read the full report which includes coverage on Credit, FX, Rates, and Thematics.

Topic

The information published by DBS Bank Ltd. (company registration no.: 196800306E) (“DBS”) is for information only. It is based on information or opinions obtained from sources believed to be reliable (but which have not been independently verified by DBS, its related companies and affiliates (“DBS Group”)) and to the maximum extent permitted by law, DBS Group does not make any representation or warranty (express or implied) as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions and estimates are subject to change without notice. The publication and distribution of the information does not constitute nor does it imply any form of endorsement by DBS Group of any person, entity, services or products described or appearing in the information. Any past performance, projection, forecast or simulation of results is not necessarily indicative of the future or likely performance of any investment or securities. Foreign exchange transactions involve risks. You should note that fluctuations in foreign exchange rates may result in losses. You may wish to seek your own independent financial, tax, or legal advice or make such independent investigations as you consider necessary or appropriate.

The information published is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction; nor is it calculated to invite, nor does it permit the making of offers to the public to subscribe to or enter into any transaction in any jurisdiction or country in which such offer, recommendation, invitation or solicitation is not authorised or to any person to whom it is unlawful to make such offer, recommendation, invitation or solicitation or where such offer, recommendation, invitation or solicitation would be contrary to law or regulation or which would subject DBS Group to any registration requirement within such jurisdiction or country, and should not be viewed as such. Without prejudice to the generality of the foregoing, the information, services or products described or appearing in the information are not specifically intended for or specifically targeted at the public in any specific jurisdiction.

The information is the property of DBS and is protected by applicable intellectual property laws. No reproduction, transmission, sale, distribution, publication, broadcast, circulation, modification, dissemination, or commercial exploitation such information in any manner (including electronic, print or other media now known or hereafter developed) is permitted.

DBS Group and its respective directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned and may also perform or seek to perform broking, investment banking and other banking or financial services to any persons or entities mentioned.

To the maximum extent permitted by law, DBS Group accepts no liability for any losses or damages (including direct, special, indirect, consequential, incidental or loss of profits) of any kind arising from or in connection with any reliance and/or use of the information (including any error, omission or misstatement, negligent or otherwise) or further communication, even if DBS Group has been advised of the possibility thereof.

The information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation. The information is distributed (a) in Singapore, by DBS Bank Ltd.; (b) in China, by DBS Bank (China) Ltd; (c) in Hong Kong, by DBS Bank (Hong Kong) Limited; (d) in Taiwan, by DBS Bank (Taiwan) Ltd; (e) in Indonesia, by PT DBS Indonesia; and (f) in India, by DBS Bank Ltd, Mumbai Branch.