- Banking

- Wealth

- Privileges

- NRI Banking

- Treasures Private Client

- 2024 marks the start of the next semicon upcycle, driven by double digit growth in logic and memory

- Strong surge in semiconductor M&A deals YTD reflects growing trend of vertical integration

- Semiconductor industry will continue to reap benefits from AI

- Strong capex trends and rising productivity are positive signs for profitability

- Continue to favour semiconductor leaders on the growth end of the CIO Barbell strategy

Related Insights

- DBS Stock Pulse: (1) Aztech cut to Fully Valued on weak outlook (2) Equity picks – Raise exposure to Starhill Global30 Oct 2024

- Equity Strategy | AI Commercialisation to Drive Next Leg of Tech Boom (Part 3 of 3) 29 Oct 2024

- DBS Stock Pulse: Japfa’s strong 3Q results likely seals the deal for solid full-year earnings29 Oct 2024

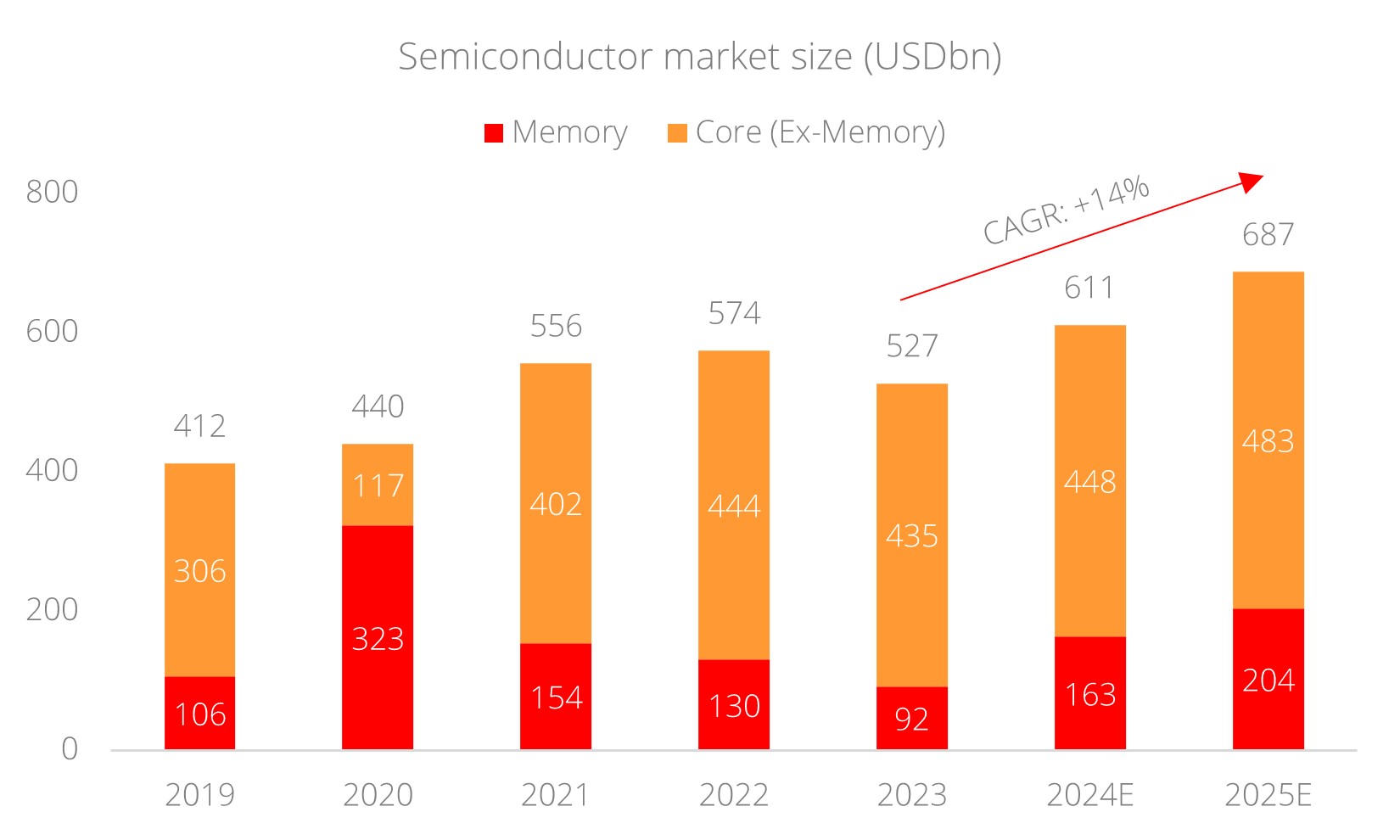

Paving the way for a stronger upcycle. After a challenging 2023, the semiconductor industry is on track to rebound strongly, driven by strong expansion in AI semiconductor demand. Marked by double digit growth in the logic and memory segments, the total semiconductor market is expected to grow 16% this year to reach USD611bn. The need for cutting-edge, AI-enabling graphics processing units (GPUs) remains stronger than ever, supported by strong demand among cloud hyperscalers and datacentre providers. The memory segment, which is key to the storage and access of information for datacentres, is expected to grow a stellar 77% this year as it rides on the AI-led datacentre boom. Consequently, semiconductor stocks have done well this year, with leading AI chip companies like NVIDIA rallying 174%, while the broader semiconductor industry rose 60%, outperforming both Big Tech (+33.8%) and the broader market (+17.2%) on a YTD basis.

M&A activity heating up. The semiconductor industry is seeing bustling M&A activity this year. As at end August, there have been a total of 44 deals in the semiconductor space, 33% higher than last year. More importantly, the total deal value of M&A transactions this year saw a 16x increase from last year (USD45.4bn vs USD2.7bn). This substantial rise in deal value was driven by two deals: Synopsys’ acquisition of Ansys (USD35b) and Renesas’ acquisition of Altium (USD5.9bn). These two transactions reflect a larger trend of semiconductor processor companies acquiring non-chip companies (e.g. software developers), to enhance their AI platforms and high-performance computing capabilities. NVIDIA announced four acquisitions this year related to embedded AI software, which will enhance their capabilities in compute unified device architecture (CUDA) and foster larger ecosystems around their GPUs. AMD also announced two acquisitions to bolster its server building (ZT Systems) and AI platform (Silo AI) capabilities. This trend of vertical integration shows how leading semiconductor companies are actively looking to expand their technological capabilities and capacity, and constantly positioning themselves to capture a larger end market. The adage “victory begets victory” very much applies to industry leaders in the semiconductor space.

Plenty of AI-driven growth ahead. Semiconductor chips are the foundation of modern technology, powering everything from smartphones and computers to medical devices and smart home systems. AI is no exception – AI models and applications require specialised semiconductor chipsets and integrated circuits to run, and the acceleration of AI adoption will see increasing demand for these chips moving forward. Considering AI is but in its nascent stages of development, it is reasonable to assume the bulk of its growth lies ahead of us. As the total addressable market (TAM) for AI grows steeply (projected to reach c.USD2.6tn by 2032), there will be a positive spillover effect on the semiconductor industry, which is seeing a rising proportion of its revenue come from AI-related end uses. Another long-term tailwind that will drive prospects for the semiconductor industry is robust global technology spending, which reached a staggering USD4.4tn in 2023. To put things into context, that amount is larger than the entirety of Japan’s GDP in the same year.

Robust capex and rising productivity. The AI-led growth wave in the semiconductor industry will be enhanced by robust capital expenditure (capex) from tech firms with deep pockets. Research and development will ensure a strong pipeline of chipsets from integrated circuit (IC) design companies while spending to diversify and shore up manufacturing capacity by foundries will ensure supply can keep up with growing demand. The sector’s healthy investment has also brought about a steadily rising level of productivity; revenue per 1,000 employees reached USD500mn in 2023, up from just USD60mn in the mid-1980s. This is a positive sign that profitability within the sector will remain buoyant.

Stay invested in semiconductor leaders. We continue to advocate for exposure to the semiconductor space, particularly the sector leaders, to be on the growth end of the CIO Barbell strategy for their structural criticality to modern technology and ever-expanding addressable market. The industry has and will continue to benefit from the transformative effects of AI for a long time to come. Revenue-per-share for the industry is at multi-year highs, reflecting its strong growth trajectory. On a growth-adjusted basis, valuations for semiconductor players remain undemanding; the two-year average (2024 and 2025) PEG ratio for the industry is a substantial 1.7x lower than global equities’ 2.9x. As the hype around AI gradually fades, it is useful to consider Amara’s law, which states that we often overestimate a technology's short-term effects while underestimating its long-term impact when considering the investment case for semiconductor players and AI beneficiaries. While short-term market fluctuations may be tempting to react to, the true attractiveness of semiconductor and AI investments lie in their potential for sustained, long-term growth.

Figure 1: Semiconductors on track for a strong 2024

Source: World Semiconductors Trade Statistics, Semiconductor Market Forecast Spring 2024, DBS

Download the PDF to read the full report.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investmen. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")

Related Insights

- DBS Stock Pulse: (1) Aztech cut to Fully Valued on weak outlook (2) Equity picks – Raise exposure to Starhill Global30 Oct 2024

- Equity Strategy | AI Commercialisation to Drive Next Leg of Tech Boom (Part 3 of 3) 29 Oct 2024

- DBS Stock Pulse: Japfa’s strong 3Q results likely seals the deal for solid full-year earnings29 Oct 2024

Related Insights

- DBS Stock Pulse: (1) Aztech cut to Fully Valued on weak outlook (2) Equity picks – Raise exposure to Starhill Global30 Oct 2024

- Equity Strategy | AI Commercialisation to Drive Next Leg of Tech Boom (Part 3 of 3) 29 Oct 2024

- DBS Stock Pulse: Japfa’s strong 3Q results likely seals the deal for solid full-year earnings29 Oct 2024